UAE E-Invoicing Guidelines: What UAE Businesses Need to Know

The UAE’s new e-Invoicing Guidelines (Feb 2026) roll out a nationwide electronic invoicing system for all businesses. The initiative aligns with the UAE’s digital economy vision and promises significant benefits. According to the official guidelines, e-invoicing will maximize tax compliance and efficiency while improving transparency and taxpayer experience. Key advantages include:

Tax compliance: Maximize compliance, tackle the shadow economy, and shrink the tax gap.

Effectiveness: Increase transparency and improve audits, encouraging a long-term culture of compliance.

Taxpayer experience: Enhance taxpayer and user experiences with potentially new and innovative services.

Digitalization: Reduce manual work in business and tax reporting, making the UAE’s fiscal ecosystem more digitally enabled.

Efficiency: Optimize costs and operations, reduce processing time, and cut paper waste (supporting sustainability goals).

Economic contribution: Contribute to the growth and competitiveness of the economy and leverage big data for insights.

Support policy-making: Provide near-real-time data to policymakers, helping identify sectors needing support.

Beyond these national benefits, businesses will see easier invoicing processes (faster payments, fewer disputes, digital record-keeping) as noted in the guidelines. Overall, the system aims to streamline VAT compliance and make doing business in the UAE smoother.

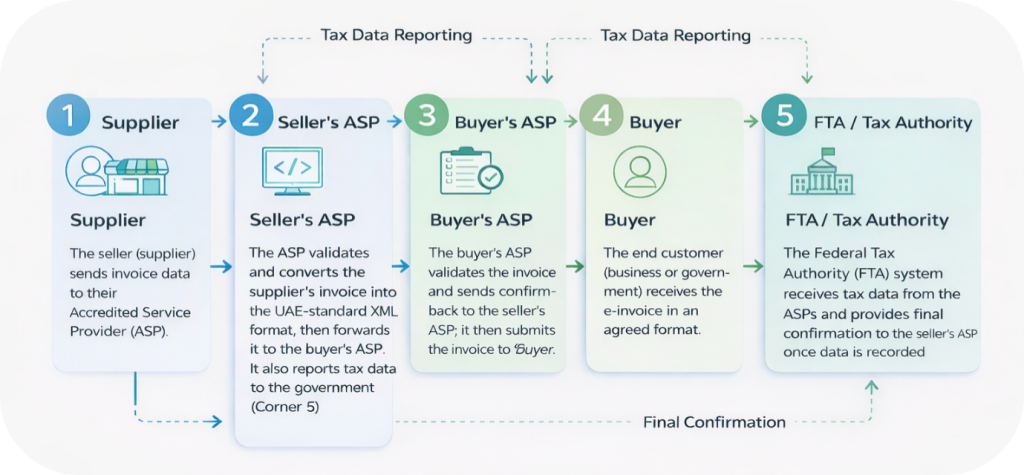

The 5-Corner E-Invoicing Framework

The guidelines describe a “5-Corner” model for e-invoice exchange. In this framework, each “corner” plays a role in transmitting, validating, and reporting invoices electronically:

Corner 1 – Supplier: The seller (supplier) sends invoice data to their Accredited Service Provider (ASP).

Corner 2 – Seller’s ASP: The ASP validates and converts the supplier’s invoice into the UAE-standard XML format, then forwards it to the buyer’s ASP. It also reports tax data to the government (Corner 5).

Corner 3 – Buyer’s ASP: The buyer’s ASP validates the invoice and sends confirmation back to the seller’s ASP; it then submits the invoice to the buyer. Upon successful validation, it reports tax data to the government.

Corner 4 – Buyer: The end customer (business or government) receives the e-invoice in an agreed format.

Corner 5 – FTA/Tax Authority: The Federal Tax Authority (FTA) system receives tax data from the ASPs and provides final confirmation to the seller’s ASP once data is recorded.

In practice, a supplier works with an ASP to issue e-invoices. The ASPs handle format conversion, validation, and secure transmission. This decentralized setup (peppol-based) enhances security and auditability, while giving the FTA the data it needs in near real-time. The chart on page 10 of the guidelines visualizes this flow, but in summary: Seller → Seller’s ASP → Buyer’s ASP → Buyer, with both ASPs reporting tax data to the FTA.

Data Storage & Archival Requirements

Under Article 3(1) of the Tax Procedures Law, all e-invoice data (issued, transmitted, received) must be retained for specified periods. Key requirements are:

5 years after the relevant tax period (for taxable persons).

5 years from end of calendar year of invoice creation (for non-taxable persons).

7 years from end of calendar year of invoice creation for real estate records.

If there is an ongoing audit or dispute, taxable persons must keep records an extra 4 years. And if a voluntary disclosure is filed in year 5, retain related records 1 additional year.

Crucially, Article 11 of the guidelines clarifies “within the State” storage: records can be on servers inside or outside the UAE as long as the FTA can access, retrieve and reproduce them electronically on demand. In other words, digital records must preserve integrity and security, and be readily available to the FTA, but cloud or offshore storage is permitted if these conditions are met.

Scope of E-Invoicing: In-Scope Transactions

E-invoicing is mandatory for all business transactions in the UAE involving businesses or government entities. The key chart on page 14 defines in-scope transaction types:

Included: B2B and B2G (Business to Business/Government), G2B and G2G (Government to Business/Government).

Excluded: B2C (Business to Consumer), G2C (Government to Consumer), and any sale to non-business consumers.

In practice, if either party to a transaction is a business or government entity, e-invoicing is required, unless specifically excluded. The guidelines state that any supply to or from a natural person (consumer) not engaged in business is out of scope. For example, sales of goods or services to private individuals (B2C) do not require e-invoices. However, goods/services sold to government entities (e.g. via UAE government procurement) are included.

VAT Groups and the 24-Month Grace Period

The guidelines emphasize that intra-group transactions are generally in scope. Transactions between members of the same VAT group are not automatically exempt. However, recognizing these are often high-volume internal flows, the UAE provides a 24-month grace period for VAT groups. From January 1, 2027, VAT group members will have 24 months during which they are not required to comply immediately for their intra-group invoices. This defers the e-invoicing obligation for inter-company transactions until after 2028, giving companies time to align systems and data.

Importantly, this grace period is purely a timing relief. Intra-group transactions remain in scope; the grace period simply delays enforcement. After the 24 months, e-invoicing applies fully to all intra-group invoices under the standard phased timeline. (Note: Outside UAE-established persons making taxable supplies to or in the UAE must also issue e-invoices for those supplies.)

Exclusions from E-Invoicing

While most B2B and B2G sales are in scope, the guidelines list a few specific exclusions (Chapter 7):

Sovereign activities (7.1): Transactions are exempt if (1) done by a Government Entity, (2) in a sovereign capacity, and (3) not in competition with the private sector. In other words, purely governmental functions (mirroring VAT law) need not e-invoice.

Airline supplies (7.2): Certain international passenger services are excluded. For example, passenger fares with e-tickets or ancillary services with electronic miscellaneous documents (EMDs) are out of scope. There is a temporary 24-month exclusion for air cargo exports (airway bills) from the mandatory e-invoicing rules.

Financial services (7.3): Financial services that are VAT-exempt under Article 42 of the VAT Regulations are excluded. Exempt financial services provided to non-residents (zero-rated exports) are also excluded. However, standard-rated financial services to residents still require e-invoices.

Ministerial discretion (7.4): The Minister of Finance can specify other exclusions in future. As noted, “Other exclusions may be added by the Minister in the future”.

These exclusions are narrow and specific. In general, any sale or service that does not meet one of the above conditions must be covered by an electronic invoice under the new system.

Phased Implementation: Pilot, Voluntary, and Mandatory Timelines

The e-invoicing rollout is phased (Chapter 8):

Pilot Phase (from July 1, 2026): The FTA will run a pilot program. Selected companies will be invited to participate, but only if they opt in in writing. Participants must then meet all technical requirements.

Voluntary Adoption (from July 1, 2026):All businesses (regardless of size) may voluntarily switch to e-invoicing from this date. Voluntary users must comply fully with technical specs, but they won’t face penalties until their mandatory date arrives. Early adopters get practice and benefit from efficiencies.

Mandatory Rollout (2027 onward): Based on revenue bands and entity type, businesses and government entities must appoint an ASP and go live on specific deadlines. Key mandatory deadlines include:

Large companies (≥ AED 50M): Appoint ASP by July 31, 2026; implement e-invoicing by Jan 1, 2027.

Other businesses (< AED 50M): ASP by March 31, 2027; implement by July 1, 2027.

Government entities: ASP by March 31, 2027; implement by Oct 1, 2027.

The guidelines strongly encourage planning ahead to avoid penalties. There is an initial voluntary onboarding window so businesses can test their systems without penalty risk. But after these dates, non-compliance can incur fines (see below).

Getting Ready for E-Invoicing

Businesses should start preparing now. Chapter 9 outlines a step-by-step readiness checklist:

Understand requirements: Review all relevant laws, Ministerial Decisions, and technical specs. Identify what changes your accounting or ERP systems need, and set a project plan for your mandatory date.

Select an ASP (Accredited Service Provider): Identify and contract with an FTA-approved ASP, onboard through the FTA’s EmaraTax portal, and obtain a Peppol participant identifier via that ASP. Working with experienced consultants can help here – for example, leveraging Digits’ technology consulting services for ERP integration and system design.

Test exchange & reporting: Agree on data formats and test end-to-end invoice transmission with your ASP. Ensure your system can send the required XML data to the ASP and receive confirmations.

Go live: Establish roles for invoice oversight and error handling with your ASP, then begin regular electronic invoicing and tax data reporting. Monitor for any issues during the live run and address them promptly.

Ongoing changes: After going live, update your ASP through EmaraTax if your circumstances change (e.g. business sold or offboarded). Maintain governance processes with your ASP.

By following these steps, businesses ensure a smooth transition. In particular, partnering with knowledgeable IT/consulting firms (such as Digits Technology Consulting) can help streamline ERP upgrades, integration with ASP platforms, and training of staff.

E-Invoice Categories

The guidelines define 6 categories of electronic documents (page 22). These cover standard and self-billing scenarios:

Electronic Tax Invoice: The standard e-invoice issued by a supplier (for taxable sales).

Self-billed Electronic Tax Invoice: An e-invoice issued by the buyer on behalf of the supplier (common in agency/consignment arrangements).

Electronic Tax Credit Note: A credit note issued by the supplier to correct or refund a Tax Invoice.

Self-billed Electronic Tax Credit Note: A credit note issued by the buyer for the supplier (self-billing).

Commercial Invoice: An invoice for supplies that do not require a tax invoice (e.g. zero-rated exports, exempt sales).

Electronic Credit Note: A credit note for a Commercial Invoice (non-VAT line items).

Every provisional invoice should also be in electronic form – any adjustments are handled by adding an e-Credit Note or additional e-Invoice. There is no special “provisional” category; provisional amounts follow these rules.

E-Invoicing Scenarios: Examples

The guidelines detail special scenarios where specific fields or rules apply. Three examples:

Free Zone transactions: If a transaction involves a Free Zone entity or the supply occurs within a Free Zone, the e-invoice must capture the “beneficiary” details if different from the billing party. For instance, if a supplier in a free zone sells to a mainland company on behalf of another party, the invoice must show the ultimate beneficiary in addition to the customer. (In practice, the beneficiary is the end-user or consumer of the goods/services.)

Continuous/Recurring supply: Ongoing supplies (e.g. monthly service retainers, installment deliveries of materials, milestone-based contracts) are covered as normal transactions. The key is that periodic invoicing is allowed. The guideline notes that if there are retention or milestone payments, businesses should issue separate documents (like a commercial document for retained amount calculations) and only include standard VAT amounts on the e-invoices. In short, you still issue regular e-Invoices for each period; just handle retention calculations off-invoice as needed.

Exports (to outside UAE): Exports of goods or services to customers abroad require e-invoices just like any other taxable supply. For example, a UAE wholesaler exporting products to Kuwait would issue an electronic Tax Invoice for that export sale. The guidelines clarify that the VAT tax invoice (for zero-rated exports) should be issued electronically and can be provided to Customs if needed. (Note: if the export buyer has not onboarded as an e-invoicing participant, the supplier still issues an e-invoice using the special endpoint codes defined in the rules.)

These scenarios illustrate that most business cases simply use e-invoicing per the standard rules, with a few added fields or notes for special cases.

Penalties for Non-Compliance

Companies and government entities must comply with the e-invoicing rules by their deadlines. The guidelines distinguish two types of penalties on page 32:

Administrative penalties: These are fines under the existing VAT law and Tax Procedures Law for failing to issue or maintain tax invoices properly. For example, if a business fails to issue a compliant invoice when required, they can face the usual VAT penalties (as per Cabinet Decision 40 of 2017). The key is that normal VAT invoicing rules still apply even under the e-invoicing regime.

E-Invoicing penalties: A new set of penalties (under Cabinet Decision 106 of 2025) applies specifically to e-invoicing obligations. These target failures to send electronic invoices or reports per the system requirements. (The actual fines are detailed in CD 106/2025, but businesses are warned that penalties will be enforced from each entity’s mandatory implementation date.) Importantly, no e-invoicing penalties will be levied on businesses who voluntarily issue e-invoices before their mandatory date.

In summary, once an entity’s phase begins, missing e-invoicing obligations (e.g. not sending e-invoices through an ASP or not reporting tax data) can trigger both the new e-invoice fines and standard VAT penalties. It is therefore critical to meet deadlines and maintain proper electronic records.

By following the official guidelines and planning carefully, UAE businesses can smoothly transition to electronic invoicing. The move promises long-term gains in efficiency and compliance. For help with the technical side (ERP updates, system integration, ASP onboarding, etc.), technology consulting partners like Digits can provide expert guidance.

Partner with Digits for expert support in e-invoicing readiness, from seamless ERP integration and hassle-free ASP onboarding to comprehensive compliance planning. Our Technology Consulting Services team will guide you through each step to ensure a smooth transition to UAE’s new e-invoicing requirements. Visit our Technology Consulting Services page to take the next step toward compliance success.